Casino Review of 2022

Overview

In 2022, Egamingmonitor.com scanned more than 10,000 game-page URLs from 2,400 online casinos, identifying nearly 28,000 games from 621 unique studios (belonging to 496 supplier groups). How does this compare to 2021 and what are the implications for operators, platforms and studios alike?

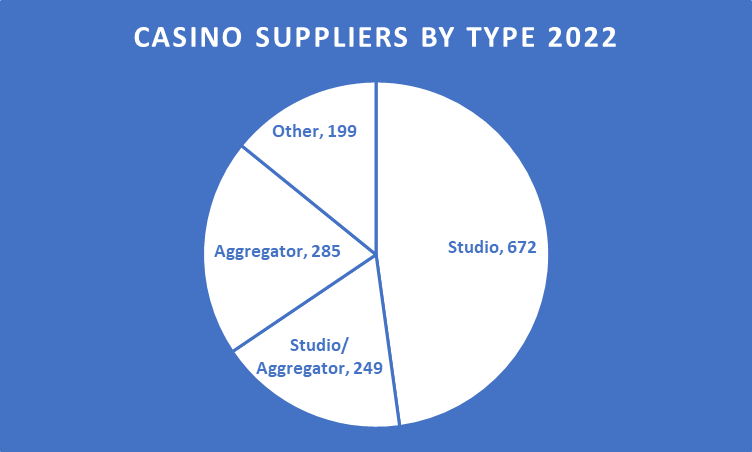

8% more suppliers than last year

The supply side of our industry grew by 8% or 100 companies in 2022 vs 2021. There are now 1,405 suppliers in the gaming world, categorised at the top level into: studios, studio/aggregators, aggregators and others.

The relative percentage by type has remained fairly constant and so just under 50 new studios, for example, were launched last year – or nearly 70 if you include the hybrid studio/aggregators. A further 24 new aggregators or platform providers entered the market too, including platforms that were spun out as B2B businesses from existing operators.

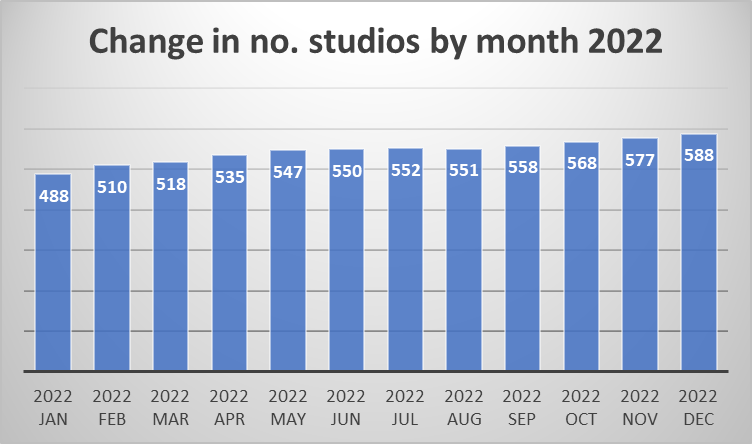

In total, we found games from 621 unique studios over the 12 months (slightly more than the December 2022 figure below as some studios may have closed or amalgamated during the period).

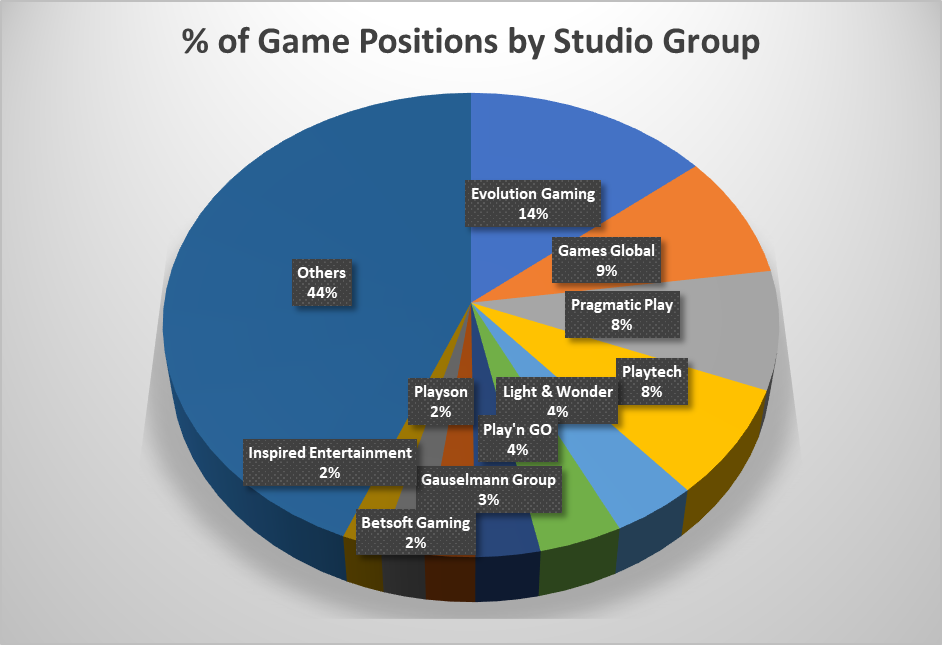

The top 10 studio groups have 56% of all game tiles globally

When we look at which studios have the best game distribution across all pages of all operator sites in 2022, the top 10 groups take up more than half of all game tiles on operator game pages. Evolution Gaming tops the list with all its subsidiaries contributing to a massive 14% of all game space across casino sites globally.

Note that on the “% of game tiles” metric, the big groups Novomatic, IGT and 1X2Network sit just outside the top 10.

If you were to rank studio groups instead by the unique number of casino sites each studio has access to, then the rankings would be similar except that Novomatic, IGT and 1X2Network would replace Inspired, Betsoft and Playson in the top 10. The difference is down to the penetration across sites: some studios may have access to more sites but others have more games per site and / or more games across multiple subpages on sites.

Evolution Gaming tops the board on this second KPI too, with gaming content from the group found across 2,081/2,459, or 85% of all casino sites globally.

| Supplier Group | No. sites rank |

| Evolution Gaming | 1 |

| Games Global | 2 |

| Pragmatic Play | 3 |

| Light & Wonder | 4 |

| Playtech | 5 |

| Play’n GO | 6 |

| IGT | 7 |

| Gauselmann Group | 8 |

| 1X2 Network | 9 |

| Novomatic | 10 |

Consolidation of content supply reaches 70%

This next chart gives a feel for the consolidation of studio content in our industry. Game content supplied by larger groups now accounts for 70% of all content on casino sites and the number is still rising. Yes, there were another 100 new studio entrants to the market last year but the share of the big incumbents continues to grow.

Note that games from “large groups” here are defined as those produced by studios that either have subsidiaries or parent companies.

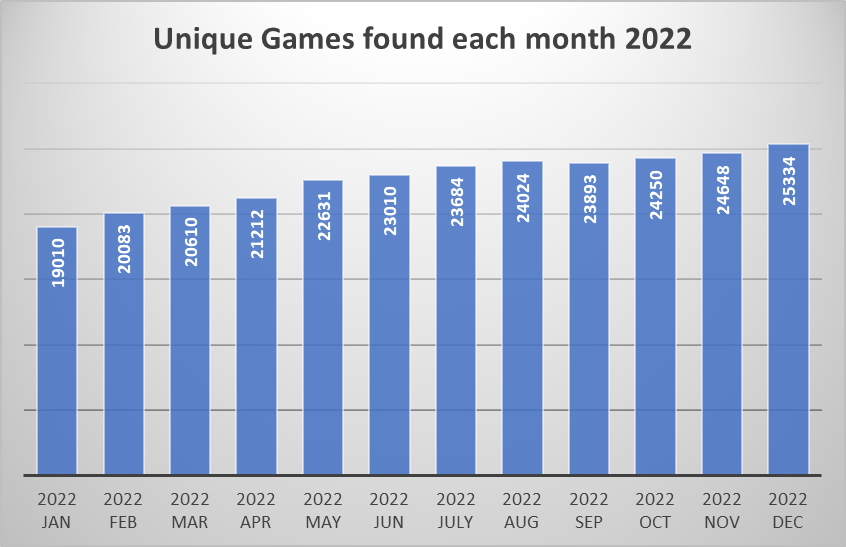

33% more games across casino sites vs 2021

We identify more than 25,000 unique games each month across operator sites, up 33% from this time last year. The sheer number of games found across operator sites has increased further – and for a handful of reasons:

a) operators do not tend to retire games

b) operators add more content studios each year either directly or via aggregators

c) aggregators add more studios to their portfolios each year (see later)

d) there are another 100 new studios this year producing content.

6,780 games were launched in 2022

Egamingmonitor adds more than 550 new games to the database each month from over 600 studios. The average studio launches just under one game per month.

| Game production stats | 2022 | 2021 |

| Avg games launched per month | 565 | 470 |

| Total studios with live games | 621 | 512 |

| Avg games launched per studio per month | 0.91 | 0.92 |

Some studios are more prolific than others. Our table of top game producers by studio group (not studio brand as such) shows how seven groups are launching more than 100 games per year. Note that this includes all game types including table games, instants, live games and so forth. Games Global’s family of studios tops the list in terms of output, closely followed by Spinomenal. While a little less familiar, two studios which focus on offshore operators, Inbet Games and KA Gaming, are highly productive.

| Supplier Group | No. games produced 2022 |

| Games Global | 186 |

| Spinomenal | 178 |

| Pragmatic Play | 165 |

| Evolution Gaming | 155 |

| Playtech | 138 |

| KA Gaming | 136 |

| Skywind Group | 111 |

| Inbet Games | 94 |

| Light & Wonder | 93 |

| IGT | 86 |

There are more than 50 studio groups building at least two games per month, i.e. 25+ per annum, while the “median average” is around seven games per studio per year.

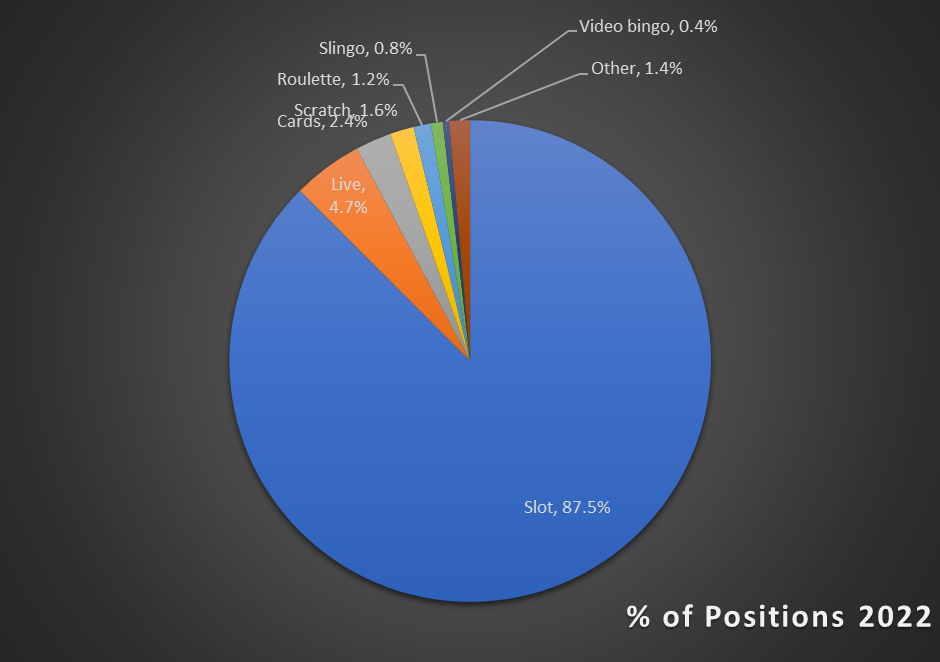

Slots make up 87.5% of all game content on operator pages

Across the 2,500 operator sites that we monitor, slots account for 87.5% of all game content across casino pages. Live games in the second spot account for around 5% of all game content on the page.

New game types such as slingo and crash games are making inroads yet are still dwarfed in numbers (the 55 crash games that exist, for example, are 0.1% of 43,000 total games on our database). Some of the more innovative games though, while taking up a very small % of total “shelf space”, are quite well distributed in terms of the number of sites where found. They also tend to be more prominent in the better page positions, i.e. nearer the top or in the new, featured or popular sections.

Operators now have games from 50 studios on their site on average

On average, operators have added another 14 studios worth of content this past year and now offer content from 50 suppliers. Note though that the median is around 35.

If each studio were to produce just under one game per month then the average number of new games that an operator could choose to launch each month would be around 45, or one and a half new games every day. The fleeting nature of novelty is more evidence that the lifespan of games is shortening yet further.

| Operator x game/studio stats | 2022 | 2021 |

| Avg games on an operator’s site | 650 | 545 |

| Avg no. of studios on an operator’s site | 50 | 36 |

| Games launched per month per operator* | 45 | 39 |

| Any new game % of all new games on operator site | 2% | 3% |

| Any new game % of total games on operator site | 0.2% | 0.2% |

| Most studios per site | 257 | |

| % of sites that have >100 studios | 16% |

A handful of operators offer over 4,000 games on site

The largest operators in terms of breadth of game content include the likes of Videoslots.com plus sites licensed in Curacao by the likes of Altacore, Avento and Equinox. 16% of all operator sites offer games from more than 100 studios.

Meanwhile, there are also some operators who no longer add all content from all suppliers but instead focus on relevance and quality rather than quantity.

Starburst still no. 1 – the consolidated 2022 chart…

In terms of distribution, Starburst still ranks no. 1 globally on our games chart for 2022, and the game is found across 1,395 sites or 56% of the total. See our January dashboard for December’s chart. The groups Evolution Gaming, Pragmatic Play, Games Global and Play’n GO dominate the top 20 positions. Note that the chart below also includes non-slots content, with live games Crazy Time and Lightning Roulette also making it into the top 20. The top new games this past year were Bigger Bass Bonanza, Big Bass Splash and Gates of Olympus from Pragmatic Play plus Dynamite Riches Megaways from Red Tiger.

| Game (Studio) | Rank |

| Starburst (NetEnt) | 1 |

| Big Bass Bonanza (Pragmatic Play) | 2 |

| Book Of Dead (Play’n GO) | 3 |

| Lightning Roulette (Evolution Gaming) | 4 |

| Sweet Bonanza (Pragmatic Play) | 5 |

| Gates of Olympus (Pragmatic Play) | 6 |

| Bonanza (Big Time Gaming) | 7 |

| Wolf Gold (Pragmatic Play) | 8 |

| Bigger Bass Bonanza (Pragmatic Play) | 9 |

| Dynamite Riches Megaways (Red Tiger) | 10 |

| Gonzo’s Quest (NetEnt) | 11 |

| Gonzo’s Quest Megaways (Red Tiger) | 12 |

| 9 Masks Of Fire (Gameburger Studios) | 13 |

| 9 Pots Of Gold (Gameburger Studios) | 14 |

| The Dog House Megaways (Pragmatic Play) | 15 |

| Legacy Of Dead (Play’n GO) | 16 |

| Wild Wild Riches (Pragmatic Play) | 17 |

| Big Bass Splash (Pragmatic Play) | 18 |

| Crazy Time (Evolution Gaming) | 19 |

| Immortal Romance (Microgaming) | 20 |

Branded games are on the wane but high volatility Animals & Nature titles on the up!

It’s worth throwing out a few interesting stats relating to game features from 2022. Branded games are a smaller percentage of all game content this past year vs 2021, while Megaways are slightly up.

The top themes of 2022 were Action & Adventure, Tales & Legends and Animals & Nature. The themes Animals & Nature and Tales & Legends in particular, increased their share of game distribution globally.

The most popular game words in 2022 were: Hot, Fruit, Fortune, Dragon, Gold, Wild, Gods, Magic and Megaways.

And the winner of “Colour of the Year” is… brown

Not exactly the most exciting tint perhaps, but brown is the colour that has increased its share most, across the billions of pixels of game-tiles out there!

| Game feature stats | 2022 | 2021 |

| % Ways | 1.7% | 1.6% |

| % using licensed third-party brands | 2.2% | 2.5% |

| RTP | 95.3% | 95.4% |

| Med vol % | 35.7% | 36.9% |

| High vol % | 28.4% | 27.4% |

| 5 Reels % | 80.9% | 82.7% |

| Action & Adventure | 10.5% | 10.3% |

| Tales & Legends | 6.7% | 5.3% |

| Animals & Nature | 5.3% | 4.1% |

| Black | 34.3% | 34.6% |

| Brown | 22.6% | 22.3% |

| Silver | 11.8% | 11.9% |

Top dealmakers 2022

The aggregator 1Click Games was the busiest aggregator in 2022 in terms of integrating new content partners – one reason, perhaps, why they were recently acquired by crypto platform Lion Gaming. They struck deals with 27 studios in the year, well ahead of second and third place PariPlay and Relax Gaming. EveryMatrix remains the most “connected” aggregation platform of all time with casino content sourced from a massive 217 studios.

The busiest studio over the last 12 months from a deals perspective was the live games supplier Beter, which managed to secure six distribution deals via aggregators. Apparat Gaming, CT Gaming, Lady Luck Games, Slotmill and Spribe were all close runners-up.

And finally, originality is on trend. Only 11% of games launched in 2022 had the same name

A little-known fact: historically, 15% of all slot games have the same name as another. But there was an improvement this last year as just 11% of slot games launched shared names with an existing title. Football Fever was popular but it was another handful of “Cleopatra” games (adding to nine that were already out there) that surprised us. Some studios are clearly hoping that a bit of that IGT royal shine rubs off.

Egamingmonitor.com cover 44,000 games, 1,400 suppliers and 2,400 operators. For access to our interactive charts and filters by country, by page type, by studio, by operator, by page type and more, please get in touch.