The dark arts of game design

In our last series of articles, we looked at the commercial aspects of game success: game distribution and game penetration across operator sites. This next set of articles focusses on the design components of game success.

Many a game designer has found the nuances that make one game outperform another elusive, and attempts to clone the likes of Rainbow Riches or Starburst rarely exceed expectations. Even when A/B testing the same game with different background colours you can find major discrepancies.

But before delving into the ingredients of that elusive recipe, we first take a look at product strategy. Where do you stand on the dimensions of quantity vs quantity, or innovator vs follower? How do you measure game performance and is the goal itself of ‘Blockbuster success’ either realistic or desirable?

Product strategy as context

Success is about growing revenues, shareholder value and fulfilling your own potential. With limited distribution, for example, even the best games will not ‘top the charts’ as such. Over-reliance on single game brands can also be a weakness as it’s the longevity of portfolio performance that counts.

For most studios, game design considerations are about maximising performance within their own group of operators and also generating content that helps to open new doors. Innovating and refining game mechanics, themes and brands will lead to stickier content, thus more gameplay and revenues. New, interesting or stickier products also make it easier to secure more aggregator partners, more operators and better site positioning across the different subpages.

Quality vs quantity

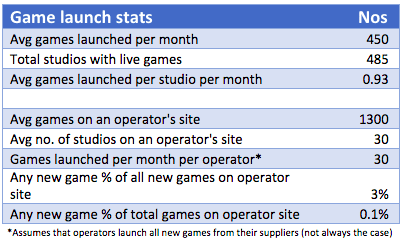

Revenues can be made up of a large volume of average games or a handful of premium titles: the usual quality vs quantity dimension. The average operator site will have around 1,300 titles from 30 studios. At Egamingmonitor we add just under 500 games from 500 studios every month to the database. In this context, being “new” is not unique or, at best, is a fleeting status.

To gain exposure you may focus on a handful of premium titles that will be featured for longer, should perform better and whose performance, in turn, will lead to improved positioning on site and thus greater longevity. Alternatively, you may try to feature in the new section more often and/or with more titles, churning out a constant stream of games, many of which may be fairly similar, at least in terms of game type and mechanics.

It’s simple maths: if the average operator adds 30 new games a month to their site and a typical studio turns out 1 game per month, then the average new release will have 3% share of exposure on the ‘new’ tab/section, or 0.1% exposure across the whole site. With the average studio fielding around 40 games in total, their share of cross-site exposure will also be 3% (40/1300).

Outside of commercial negotiations, you could improve on these ‘averages’ by producing either more, or better, games. Note that there are also hybrid models of the two, for example, whereby different sub-brands or game families are able to cover off both bases.

If a quantity strategy triumphs, then game themes and volatility levels (within the scope of existing mechanics) are the easiest components to adapt. A quality strategy meanwhile allows for more variation in game types and mechanics and can involve better graphics, animations and music, but with the obvious cost and time tradeoffs.

Among end-users, there is now a wide range of tastes for different game types, mechanics, volatility levels and themes. There are also those who value new and/or quality games more than others. When trying to appeal to these varied tastes, the same quantity/quality dimension still applies: premium games will be stickier and are likely to cater to more game type or mechanics preferences. A quantity strategy allows for broader coverage of theme interests and has a good chance at capturing those players who enjoy anything fresh and shiny.

Note that as operators tend to add games faster than they retire them (they compete with other operators on both quality and breadth of content), the maths behind this numbers game is also changing over time.

Finally, if more output is needed, your approach to in-house development vs outsourced games or game components needs some thought – but that’s one for a future article in this series.

Innovation vs tradition

Safe and solid or “out there” is a choice too. It’s related to the quality/quantity dimension since innovators tend towards quality, yet those that are less risk averse can still choose quantity over quality or vice versa.

There are costs, risks and rewards associated with innovation and where you stand on the spectrum needs to be explicit in the product strategy. It is not always either/or, either. You may straddle the two at different times, or with different studio brands or game families. You may also find your niche as a “rapid follower” of what appear to be effective innovations from the pioneers.

Data-driven product design

We all know that products are more likely to succeed if their design is driven by data. But how often do we launch products where we don’t really have enough data to hand? Internal data, market trends, competitor research, concept testing, multivariate game feature testing, customer panels or soft-launch testing with live data feedback loops. Of this list, how many of us have it all covered, or to the qualitative and quantitative level that leads to the right decisions?

If you tend to rely on internal data only, be wary of bias. Given the volatility of game engines and the behaviour of VIPs, you can find marked differences when comparing games on engagement versus financial metrics. Have you benchmarked games on revenue vs turnover vs spins vs user numbers vs returning user numbers vs session length data vs UX data? Mean or median averages can also tell a different story.

Do you have enough data to make valid conclusions? One VIP playing one game on one operator site can skew the conclusions you may draw on relative game performance. It can also impact the exposure that operators give to certain games too, leading to a vicious or virtuous circle where initial performance data leads to decisions which reinforce those same early conclusions. Similarly, recommendation engines can be overly simplistic, compounding trends based on limited data and reducing game discovery.

Looking at external data, what games or studios are ranking well? What features, themes, brands or mechanics seem to work and how does it all vary by market segment? Drilling down on game performance data by game type, by market, by feature, by theme etc. can really inform product decisions. The data also exists to see how external site distribution and positioning correlates with internal metrics.

Game components: RTP, features, mechanics, themes, colours, brands

Finally, back to the recipe, or the game components and features you choose to incorporate in a product. There are plenty of considerations here and the list below will not do them justice. Look out though for more articles in this series that consider each in turn, with data supporting the key trends.

- Game-type selection: slot, hybrid or other, such as live games, video bingo, video poker, table games, dice, keno, virtual, scratch, crash and skill games…Do you define yourselves as a slot developer or do you also cover other game types, such as table games, for example?

- Mechanics and maths engines: plenty of choices here too, including ‘ways’, clusters, slingo, reactors plus various base game vs bonus game choices. Should you develop mechanics in-house (Lock ‘n Spin, Hyperways, Quick Hits, Infinireels etc) or license those such as Megaways from third parties. If you have your own branded mechanic, should you consider licensing it to others? Mechanics and maths engines will reflect the desired volatility, RTP or hit frequencies – more on these below.

- Volatility: this is a function of payout tables, max win multipliers, jackpots and hit frequencies. Multipliers can relate to the base game, the bonus game or both. Jackpots can be fixed or progressive, single or multi-game, while Red Tiger introduced us to must-drops which can be dailies or even hourlies. Hit frequencies can be on any win, any win greater than the stake, or the frequency of triggering a bonus game. Hit frequencies can even vary by the realised RTP. Some games, for example, can auto-trigger bonus features or symbols after a long string of losses in the same session. Churn reduction is applied in real-time in the video game industry. A ‘rage algorithm’ in FPS games, for example, takes into account recent game wins and kill/death ratios, matching players to the skill level of their next of opponents based on live data. Poor recent performance leads to easier games and vice versa. There’s plenty that we can ‘borrow’ from other gaming sectors.

- Customer choices: these can be incorporated too, including those that affect volatility and hit frequencies, such as reward options or the increasingly popular feature buys, as well as the usual line number and/or bet size options. In sports betting and roulette, customers can choose long vs short odds and some slots are now facilitating these preferences within a game. Other game choices may include the ability to change ‘skins’ and/or player profiles – more functionality that is borrowed from social or video gaming.

- Skill components in slots: often touted as the crossover product between the worlds of casino gaming and social gaming, allowing players to exercise choices that represent some level of skill. As with blackjack these skill options still need to fit within the boundaries of best play RTPs. Most blackjack games have a theoretical RTP of 98-99% based on best play, for example, though they tend to realise around 95% in practice…

- RTP: is typically fixed and based on millions of gameplays but can also vary according to customer choices and game session performance as above.

- Reels, rows and layouts: very much a function of the maths engine and can be simple or complex.

- Social, gamification and multiplayer components: these include missions, tournaments, leaderboards and pooled or syndicated jackpots. These components can be either single game, multi-game or at a multi-studio level. Where functionality is platform-wide it is driven more by the aggregator or operator and studios would instead enable/adapt the functionality for their games.

- Game speed: there are conflicting trends here with compliance pressure towards minimum spin durations and the younger generation is used to shorter cycles. Sports betting has moved from pre match markets to multiple in-play events. There are also churn considerations here since games that play through funds faster run a greater risk of customer burn-out. Turboplay, autoplay and auto-reveal options all fall under this category.

- Themes, symbols, game names and colours: plenty of choices here and a review of game performance by theme by market can be informative. Egamingmonitor categorises all games into 70 themes and 20 colours – used by studios for product research and by aggregators or operators for game recommendation engines.

- Brands: studios can look to third party brands such as Monopoly and King Kong (3% of all games use licensed content) or develop their own in-house brands/brand families such as “Book of..”, “Age of The Gods” and so forth. Game brand extensions are also discussed in this context later in the series.

- Graphics, animations and music: these all contribute to the immersive gaming experience and reflect earlier decisions on target markets and themes. Note that outsourcing can work well here too.

- Game download size: speed considerations may come into play, especially with desktop vs mobile and full screen vs mini game dimensions.

A key process in product development is to segment users and to design products for specific target markets.

Segmentation can be based on demographics: age, geographic, socio-economic, but also behavioural: whether a core interest is sports, casino or bingo; online or offline; new or existing customer; VIP or recreational; plus segments based on game types, theme, game mechanic, volatility or motivation preferences.

Segmenting by motivation in particular can allow you to match the game components above to what really drives players to try out games. Motives may include entertainment, excitement and stimulation; achievement, progression and learning; escape and relaxation; or social interaction.

Then of course there are different expectations of risk/reward ratios. A big matrix of segments, drivers and their matching features or components goes a long way to defining your product strategy.

Finally, game components may need to be flexible – even for the same game – to meet different market segment requirements, whether driven by compliance needs or customer preferences. The recent German tax on stakes is but one example here.

With a clear strategy, some great distribution for your products and great relationships all securing you prominent positions across operator pages, a focus on product strategy is next. After all, even with good exposure, the games themselves still need to perform…

Kevin is the co-founder of eGaming Monitor. He was previously CEO of Gameaccount (now GAN plc) and CMO at Eurobet, Sportingbet and Betfair. Egamingmonitor.com is an advisory firm to the gambling industry, with proprietary data covering 30,000 games from 1,000 suppliers across 1,000 operator sites.

Photo by Junior Teixeira from Pexels